Overview: Revenue Options and Reforming the Tax Code

Comments for the Record

United States

Joint Select Committee on Deficit Reduction

Overview: Revenue Options and Reforming the Tax Code

Thursday, September 22 2011

By Michael Bindner

Center for Fiscal Equity

Chairwoman Murray and Vice Chairman Hensarling, thank you for the opportunity to address this topic.

The Center for Fiscal Equity has a four part proposal for long term tax reform, which will be familiar to members and staff from the House Ways and Means and Senate Finance Committees who have read our comments over the last several months. The key elements are

- a Value Added Tax (VAT) that everyone pays, except exporters,

- a VAT-like Net Business Receipts Tax (NBRT) that is paid by employers but, because it has offsets for providing health care, education benefits and family support, does not show up on the receipt and is not avoidable at the border,

- a payroll tax to for Old Age and Survivors Insurance (OASI) (unless, of course, we move from an income based contribution to an equal contribution for all seniors), and

- an income and inheritance surtax on high income individuals so that in the short term they are not paying less of a tax burden because they are more likely to save than spend – and thus avoid the VAT and indirect payment of the NBRT.

A Value Added Tax can be adjusted at the border by exempting payment for exports and fully taxing imports. The VAT can replace payment of low-rate income taxes, should be receipt visible for consumers and should be set aside to fund discretionary domestic military and civil spending. The receipt visibility allows more informed decisions by those who advocate discretionary spending programs and the public at large. Changes to trade policy implicit in enacting a VAT will more than offset any job losses caused by decreased discretionary spending – and the impact of tax increases is minimal if VAT enactment offsets a portion of income tax collections.

The NBRT base is similar to a Value Added Tax (VAT), but not identical. Unlike a VAT, an NBRT would not be visible on receipts and should not be zero rated at the border – nor should it be applied to imports. While both collect from consumers, the unit of analysis for the NBRT should be the business rather than the transaction. As such, its application should be universal – covering both public companies who currently file business income taxes and private companies who currently file their business expenses on individual returns.

The NBRT would replace payroll taxes for Hospital Insurance, Disability Insurance, Survivors Insurance for spouses under 60, Unemployment Insurance, the Business Income Taxes, on corporations, business income taxes now collected under the personal income tax system, as well as most of the revenue collected under the personal income and inheritance taxes, less the amount collected under a VAT. The health insurance exclusion now included in the Business Income Tax and other subsidies under the Affordable Care Act. Most importantly, it would fund an expanded and refundable Child Tax Credit.

In the long term, the explosion of the debt comes from the aging of society and the funding of their health care costs. Some thought should be given to ways to reverse a demographic imbalance that produces too few children while life expectancy of the elderly increases.

Unassisted labor markets work against population growth. Given a choice between hiring parents with children and recent college graduates, the smart decision will always be to hire the new graduates, as they will demand less money – especially in the technology area where recent training is often valued over experience.

Separating out pay for families allows society to reverse that trend, with a significant driver to that separation being a more generous tax credit for children. Such a credit could be “paid for” by ending the Mortgage Interest Deduction (MID) without hurting the housing sector, as housing is the biggest area of cost growth when children are added. While lobbyists for lenders and realtors would prefer gridlock on reducing the MID, if forced to chose between transferring this deduction to families and using it for deficit reduction (as both Bowles-Simpson and Rivlin-Domenici suggest), we suspect that they would chose the former over the latter if forced to make a choice. The religious community could also see such a development as a “pro-life” vote, especially among religious liberals.

Enactment of such a credit meets both our nation’s short term needs for consumer liquidity and our long term need for population growth. Adding this issue to the pro-life agenda, at least in some quarters, makes this proposal a win for everyone.

The expansion of the Child Tax Credit is what makes tax reform worthwhile. Adding it to the employer levy rather than retaining it under personal income taxes saves families the cost of going to a tax preparer to fully take advantage of the credit and allows the credit to be distributed throughout the year with payroll. The only tax reconciliation required would be for the employer to send each beneficiary a statement of how much tax was paid, which would be shared with the government. The government would then transmit this information to each recipient family with the instruction to notify the IRS if their employer short-changes them. This also helps prevent payments to non-existent payees.

Assistance at this level, especially if matched by state governments may very well trigger another baby boom, especially since adding children will add the additional income now added by buying a bigger house. Such a baby boom is the only real long term solution to the demographic problems facing Social Security, Medicare and Medicaid, which are more demographic than fiscal. Fixing that problem in the right way definitely adds value to tax reform.

The NBRT should fund services to families, including education at all levels, mental health care, disability benefits, Temporary Aid to Needy Families, Supplemental Nutrition Assistance, Medicare and Medicaid. If society acts compassionately to prisoners and shifts from punishment to treatment for mentally ill and addicted offenders, funding for these services would be from the NBRT rather than the VAT.

The NBRT could also be used to shift governmental spending from public agencies to private providers without any involvement by the government – especially if the several states adopted an identical tax structure. Either employers as donors or workers as recipients could designate that revenues that would otherwise be collected for public schools would instead fund the public or private school of their choice. Private mental health providers could be preferred on the same basis over public mental health institutions. This is a feature that is impossible with the FairTax or a VAT alone.

To extract cost savings under the NBRT, allow companies to offer services privately to both employees and retirees in exchange for a substantial tax benefit, provided that services are at least as generous as the current programs. Employers who fund catastrophic care would get an even higher benefit, with the proviso that any care so provided be superior to the care available through Medicaid. Making employers responsible for most costs and for all cost savings allows them to use some market power to get lower rates, but not so much that the free market is destroyed.

Enacting the NBRT is probably the most promising way to decrease health care costs from their current upward spiral – as employers who would be financially responsible for this care through taxes would have a real incentive to limit spending in a way that individual taxpayers simply do not have the means or incentive to exercise. While not all employers would participate, those who do would dramatically alter the market. In addition, a kind of beneficiary exchange could be established so that participating employers might trade credits for the funding of former employees who retired elsewhere, so that no one must pay unduly for the medical costs of workers who spent the majority of their careers in the service of other employers.

Conceivably, NBRT offsets could exceed revenue. In this case, employers would receive a VAT credit.

The Center calculates an NBRT rate of 27% before offsets for the Child Tax Credit and Health Insurance Exclusion, or 33% after the exclusions are included. This is a “balanced budget” rate. It could be set lower if the spending categories funded receive a supplement from income taxes.

In testimony before this committee, Lawrence B. Lindsey explored the possibility of including high income taxation as a component of a Net Business Receipts Tax. The tax form could have a line on it to report income to highly paid employees and investors and pay surtaxes on that income.

The Center considered and rejected a similar option in a plan submitted to President Bush’s Tax Reform Task Force, largely because you could not guarantee that the right people pay taxes. If only large dividend payments are reported, then diversified investment income might be under-taxed, as would employment income from individuals with high investment income. Under collection could, of course, be overcome by forcing high income individuals to disclose their income to their employers and investment sources – however this may make some inheritors unemployable if the employer is in charge of paying a higher tax rate. For the sake of privacy, it is preferable to leave filing responsibilities with high income individuals.

Both the NBRT and VAT would, as consumption taxes, burden both labor costs and profit. In other OECD countries, all of whom have consumption taxes, capital gains taxes can be lower, since a portion of the taxation of capital already occurs as part of the VAT. The logic to enact lower capital gains and dividend taxes outside of a consumption tax environment is not as strong.

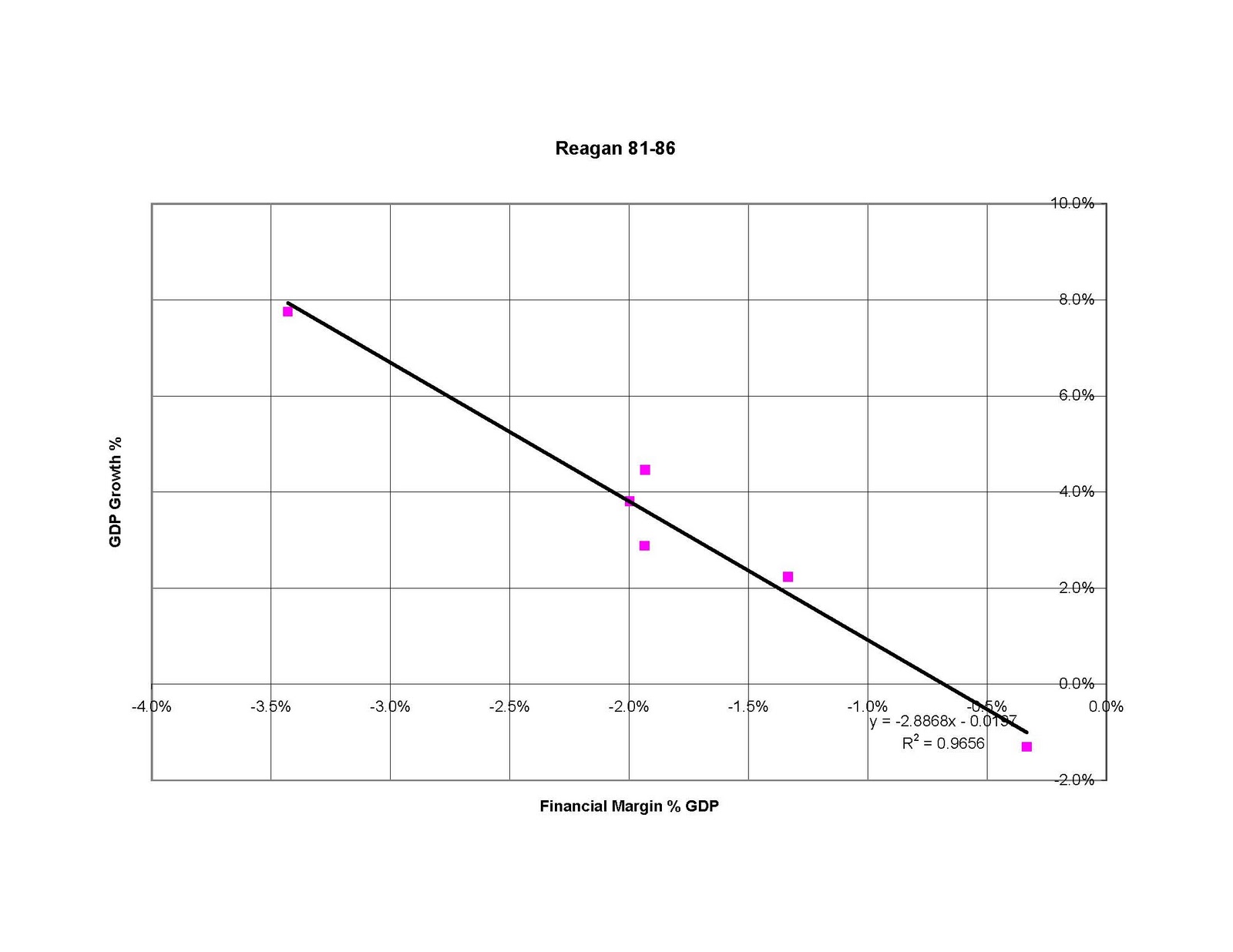

The Center for Fiscal Equity believes that lower dividend, capital gains and marginal income taxes for the wealthy actually destroy more jobs than they create. This occurs for a very simple reason – management and owners who receive lower tax rates have more an incentive to extract productivity gains from the work force through benefit cuts, lower wages, sending jobs offshore or automating work. As taxes on management and owners go down, the marginal incentives for cost cutting go up. As taxes go up, the marginal benefit for such savings go down. It is no accident that the middle class began losing ground when taxes were cut during the Reagan and recent Bush Administrations, both of which saw huge tax cuts. Keeping these taxes low is also part of why we are experiencing a jobless recovery now.

As long as management and ownership benefit personally from cutting jobs, they will continue to do so. Tax reform must reverse these perverse incentives.

In order to preserve vertical equity in a given tax year in a consumption tax environment, some form of progressive income and inheritance taxation is essential, otherwise the debt crisis cannot be avoided as consumption taxes will never be adequate to replace the lost revenue.

The Center suggests retaining surtaxes on high income earners and heirs. These would replace the Inheritance or Death Tax by instead taxing only cash or in-kind distributions from inheritances but not asset transfers, with distributions remaining tax free they are the result of a sale to a qualified Employee Stock Ownership Plan.

Retaining income surtaxes could have few rates or many rates, although we suspect as rates go up, taxpayers of more modest means would prefer a more graduated rate structure. The need for some form of surtax at all is necessary to avoid regressive tax rates in the short term, which takes into account the fact that at the higher levels, income is less likely to be spent so that higher tax rates are necessary to ensure progressivity.

This tax would fund net interest on the debt, repayment of the Social Security Trust fund, any other debt reduction and overseas civilian, military, naval and marine activities, most especially international conflicts, which would otherwise require borrowing to fund. It would also fund transfers to discretionary and entitlement spending funds when tax revenue loss is due to economic recession or depression, as is currently the case. Unlike the other parts of the system, this fund would allow the running of deficits.

Explicitly identifying this tax with net interest payments highlights the need to raise these taxes as a means of dealing with our long term indebtedness, especially in regard to debt held by other nations. While consumers have benefited from the outsourcing of American jobs, it is ultimately high income investors which have reaped the lion’s share of rewards.

The loss of American jobs has led to the need for foreign borrowing to offset our trade deficit. Without the tax cuts for the wealthiest Americans, such outsourcing would not have been possible. Indeed, there would have been any incentive to break unions and bargain down wages if income taxes were still at pre-1981 or pre-1961 levels. The middle class would have shared more fully in the gains from technical productivity and the artificial productivity of exploiting foreign labor would not have occurred at all.

Increasing taxes will ultimately provide less of an incentive to outsource American jobs and will lead to lower interest costs overall. Additionally, as foreign labor markets mature, foreign workers will demand more of their own productive product as consumers, so depending on globalization for funding the deficit is not wise in the long term.

Identifying deficit reduction with this tax recognizes that attempting to reduce the debt through either higher taxes on or lower benefits to lower income individuals will have a contracting effect on consumer spending, but no such effect when progressive income taxes are used. Indeed, if progressive income taxes lead to debt reduction and lower interest costs, economic growth will occur as a consequence.

Using an income tax to fund deficit reduction explicitly shows which economic strata owe the national debt. Only income taxes have the ability to back the national debt with any efficiency. Payroll taxes are designed to create obligation rather than being useful for discharging them. Other taxes are transaction based or obligations to fictitious individuals. Only the personal income tax burden is potentially allocable and only taxes on dividends, capital gains and inheritance are unavoidable in the long run because the income is unavoidable, unlike income from wages.

Even without progressive rate structures, using an income tax to pay the national debt firmly shows that attempts to cut income taxes on the wealthiest taxpayers do not burden the next generation at large. Instead, they burden only those children who will have the ability to pay high income taxes. In an increasingly stratified society, this means that those who demand tax cuts for the wealthy are burdening the children of the top 20% of earners, as well as their children, with the obligation to repay these cuts. That realization should have a healthy impact on the debate on raising income taxes.

If the Committee rejects consumption taxes as part of tax reform, the Center offers the following recommendations:

- End the exemption for children and increase the refundable Child Tax Credit by the same amount.

- End the mortgage interest deduction and the property tax deduction for individual homes and increase the refundable Child Tax Credit by the same amount.

- End the exemption of the blind and the elderly and replace with tax credits.

- End the taxability of Social Security benefits.

- Consolidate the 10% and 15% tax rates to a single rate.

- Increase the tax rates on capital gains and dividends and lower the Corporate Income Tax rate and the 28%, 33% and 35% rates to a single rate adequate to increase revenue by $2 Trillion over 10 years.

posted by Michael Bindner at 10:00 AM

0 comments

![]()

![]()