Economic Models Available to the Joint Committee on Taxation for Analyzing Tax Reform Proposals

Comments for the Record

House Ways and Means Committee

Hearing on Economic Models Available to the Joint Committee on Taxation for Analyzing Tax Reform Proposals

Wednesday, September 21, 2011, 10:00 AM

1100 Longworth House Office Building

By Michael G. Bindner

Center for Fiscal Equity

Chairman Camp and Ranking Member Levin, thank you for the opportunity to submit comments on these issues. The Center for Fiscal Equity feels three types of models merit attention.

The first type of model needed is a robust model for the estimation of both revenue and the impact on the economy of consumption taxes, which include the FairTax, Value Added Taxes and a VAT-like Net Business Receipts Tax. The Center for Fiscal Equity bases its estimates for VAT and NBRT revenues on estimates developed by the Brooking-Urban Tax Policy Center, which estimate that a 5% broad based VAT would raise $259 Billion after reductions in other types of revenue are factored in.

We suggest that the JCT validate this model and its sensitivity range. For example, do these estimates imply that a 10% VAT would yield $518 Billion in net revenue? Would a 25% broad based NBRT yield $1.285 Trillion? A robust set of estimates by the JTC would keep everyone on the same page in proposing various revenue options.

The second type of model needed for tax reform and deficit reduction is an estimate of the economic effects of various spending and tax benefit programs. The following questions come to mind:

- What is the impact of defense contracting versus Medicare provider payments versus the Child Tax Credit versus lower dividend tax rates?

- Do lower tax rates on the wealthy cause growth or do they provide an incentive to firms to pursue productivity gains, including off-shoring jobs, union busting and holding wages in line?

- What is the impact of these policies on the middle class?

- What is the impact of these policies on inflation?

- How do tax policies relate to the creation of asset bubbles, especially when capital gains taxes are cut, as they were in 1997, when the Technology Boom was fueled, only to be followed by the Tech Bubble popping and the 2001 recession?

- On all of these models, is there a lag effect between outlays of various types and their full impact on the economy?

- How does each type of spending effect consumption, savings and investment?

- What are the secondary effects as households and firms then spend the money they receive, including the effect on federal and state revenues?

- Is aerospace procurement more likely to stimulate spending the, for example, a tax cut to aerospace executives?

- How does each affect investment in both plant and equipment and in the secondary markets?

The third type of model relates to how deficit financing effects economic growth rates in the aggregate. With a large debt, are deficits partly offset by outlays for net interest, with the size of the deficit being offset by such outlays when they are approximately equal? How do these effects relate to tax policy? When tax policy is more progressive, yielding more revenue from wealthier taxpayers, is budget balancing stimulative? When tax rates are cut and revenue falls, are deficits required to keep money in circulation?

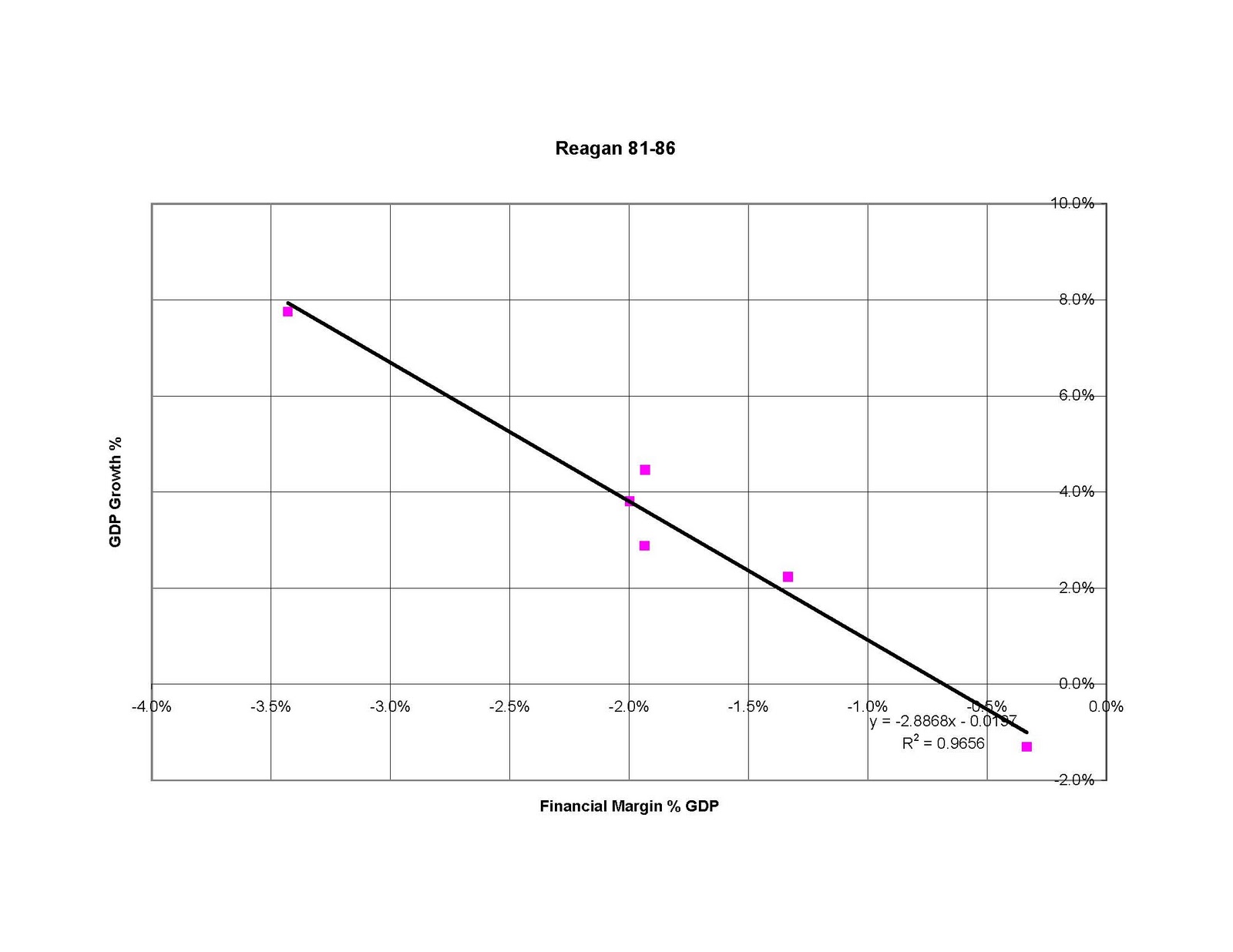

The Center for Fiscal Equity has developed figures relating to the third model, which we call the financial margin, where the financial margin is the deficit/surplus added to outlays for net interest, all expressed as a percentage of Gross Domestic Product (GDP) and regressed onto growth in real GDP in the next year, removing inflation from the analysis. See the following table for the data set used in these analyses. (Click on image to see larger text).

This repeats a study we performed but did not publish in 1987, which showed that Republican administrations generally must run bigger deficits to yield economic growth, but Democratic administrations generally did not. Indeed, these administrations had better economic performance by raising marginal tax rates on wealthier households.

For the Eisenhower years, roughly fiscal year 1954 – 1960, budget results predict growth in 1955-1961.The model explains 47% of the variation of the data and predicts a base growth rate of 4.1% with a 1.38% less growth for every 1% of GDP decrease in the financial margin – meaning that deficits were necessary to keep growing the economy. While tax rates were high, these rates were not designed to raise revenue, but to assure that middle class jobs were preserved.

The Kennedy and pre-war Johnson years show a much different picture. In a model which explains 98% of the variation, 3.13% of growth results from every 1% increase in the financial margin, with a base growth rate of 4.2%. In other words, paying back debt led to more growth.

The postwar model explains 66% of the variation, with a base growth rate of 0.2% and 2.3% of growth resulting from every 1% decrease in the financial margin, showing deficit spending was necessary to yield growth in the economy.

For the Reagan-Bush years as a whole, the model explains 37% of variation for the period 1981-1992, with a base growth rate of 1.4% and 1.3% of additional growth resulting from every percent GDP of deficit spending net of net interest. Isolating 1981-1986 yields a model which explains 96% of the variation. With a base growth rate of -2.0 %, 2.9% of growth is produced for every one percent of GDP decline in the financial margin – meaning budget balancing hurt the economy and deficits were necessary to grow it.

When George H.W. Bush and Bill Clinton raised taxes and controlled spending, more growth resulted, with 0.33% of growth resulting from each additional percentage of debt reduction, in a model that explains 72 percent of the variation, with a base growth rate of 3.4%.

The curve changes to negative once fiscal policy changed direction. In a model that explains 57% of the variation and a base growth rate of 2.4%, achieving a 1% growth rate requires an additional 0.27 percent of GDP loss in the financial margin – meaning the anemic growth of the last decade was fueled by deficits.

We believe that a Keynesian relationship explains these findings. When fiscal policy in the aggregate takes more money out of the bond markets after taxes have been cut, the running of deficits (net of interest payments) reduces savings and increases consumption by both the government and households.

When budget balancing using tax increases aimed at lower wage workers occurs, such as an increase in the payroll tax or “sin taxes” or through cuts to spending, such as Gramm-Rudman-Hollings, and deficits are smaller compared to net interest, the economy contracts as the savings sector on average increases at the expense of both government and household spending.

When budget balancing occurs because of higher marginal tax rates, however, money is removed from the savings sector in comparison to the consumption sector, making more credit available as well as higher government and household consumption.

This is essentially what happened when Presidents Bush and Clinton raised taxes in the 90s. Even though the budget neared and achieved balance, consumption continued in both the government and household sectors, although there were cuts, both absolute and programmatic, in the defense sector, while credit was widely available. When capital gains tax rates were cut in 1997, however, the savings sector received a greater share of output, resulting in an investment boom which we now know exceeded the availability of high value investment opportunities, driving up both asset prices and allowing junk investments to enter the market, which could not provide adequate returns in most cases, causing the 2001 recession.

The tax cuts of 2001 and 2003 reduced revenue and increased deficits to record levels in the post-war era, with further asset inflation leading to the current economic depression, especially in the housing market.

This brings us to the current economic situation. The Great Recession as obviously shifted the Financial Margin curve. While the current curve has few data points, these observations are consistent with both theory and economic data in the post-war era.

The Joint Committee on Taxation is urged to examine this model, as it has major implications for the road forward. Cutting the budget too aggressively could result in disaster, however allowing the Clinton tax rates to expire may allow the economy to return to the curves experienced in the early 1960s or the 1990s.

Our comments raise serious issues that must be dealt with in determining fiscal policy in the near term. Further adherence to current tax policy may lock us into a model where unsustainable debt is necessary to sustain the economy. Finding a way out of this debt by reverting to a more rational tax policy, based on these data, is essential.

Thank you again for the opportunity to present our comments. We are always available to members, staff and the general public to discuss these issues.

posted by Michael Bindner at 10:02 AM

![]()

![]()

0 Comments:

Post a Comment

<< Home