Finance: Anti-Poverty and Family Support Provisions in the Tax Code, June 14, 2023

These comments restate those made to the Ways and Means Work and Welfare Committee in March regarding work requirements. As you might guess from our prior comments from the record, we challenged the main assumption of the hearing.

WM Work and Welfare: Welfare is Broken: Restoring Work Requirements to Lift Americans Out of Poverty, March 29, 2023

The short answer to using work to lift families out of poverty is to make work pay, which sounds like a good topic for a hearing before this Subcommittee. Indeed, there is a term for making people go to work for inadequate pay: slavery.

First and foremost, wages must be adequate. In 2021, the House proposed increasing the minimum wage to $15 per hour as part of reconciliation. Until the Senate Parliamentarian ruled that this was out of order and the votes did not exist to overrule her, the Republican Minority counter-offered a $10 per hour.

American workers would appreciate putting that counter-offer back on the table, while ending the tipped wage subminimum rate. American customers are not nearly generous enough for this to be at all just. Wherever either (or both) options are proposed as ballot initiatives, they pass. In some states, higher minimums have been enacted and more economic activity, rather than less, has occurred. The reason is obvious - when lower income people have more income they spend it all back into the economy. When wealthier people get a tax cut, they take it out of the economy and into Wall Street speculation. The sad irony is that it is in the so-called “Red States” where the minimum wage has not been raised where the economy lags.

Franchise holders have a history of paying low wages and justifying their opposition to wage increases because their wages would be squeezed out. This is not the case because, again, sales will increase to compensate. That being said, the conditions of franchise employment and franchise agreements deserve attention, as well as the tactic of using the franchise system to avoid unionization and paying for such things as health insurance. If the onus on providing health care and voting for representation is shifted to the franchisor, some firms will decide that turning franchise and gig employment into full-time employment is better. That would be a socially desirable outcome.

The second way to make work pay is to increase the already existing Child Tax Credit. To increase the incentive to work and grow the economy, the credit must be made fully refundable. People do not seek out low wage jobs because the credit is too generous. Just the opposite is true. When family wages are adequate, people make investments in themselves, like further education and skills training, so that they can move up the economic ladder.

The President’s Budget proposes that the Child Tax Credits enacted as part of the American Recovery Plan Act be restored. During that period, payment of the child tax credit was in advance of the annual tax filing. This is appropriate and will change the culture of such credits, which should be for continuing support, not an annual bonus.

We agree with increasing the CTC to at least American Rescue Plan Act levels and refundability. We would make it $1,000 per month and phase it out from the median income to the 90th percentile. During the pandemic, the IRS managed payments. This had the “stink of welfare” that even some Democratic Senators objected to, which led to its discontinuance.

I submit that, over the long-term, it would be more acceptable to distribute them either through other government subsidies, such as Unemployment Insurance, Disability Insurance, or a training stipend OR through wages.

For middle income taxpayers whose increased credits are less than their annual tax obligation, a simple change in withholding tables is adequate. Procedures are already in place to deliver refundable credits to larger families.

Employers can work with their bankers to increase funds for payroll throughout the year while requiring less money for their quarterly tax payments (or estimated taxes) to the IRS. The main issue is working out those situations where employers owe less than they pay out. This is especially true for labor intensive industries and even more so for low wage employers. A higher minimum wage would make negative quarterly tax bills less likely.

Tax reform can be used to facilitate this process. Instead of having each family file to collect their child tax credits and EITC (as an end of the year bonus), enact an employer paid subtraction value added tax and make child tax credits and health insurance tax benefits an offset to the payment of this tax and remove most families from having to file at all. Tax offsets could also be created to fund paid family medical leave, sick leave and childcare provided through employers.

Please see the attachment for the latest details of our tax reform plan. This approach is superior to the prebate mechanism proposed for the Fair Tax and for the same reason. The government should not be the national paymaster for every family.

When I graduated from Loras College and began graduate studies at the American University, the Washington Area Consortium of Universities held a conference on poverty. Every speaker in every topic area cited education as the key avenue to upward mobility.

Poor people need to work longer hours to make ends meet. Their opportunity costs to seek education are, therefore, high because education cost is competing with food and shelter (both of which are inadequate for workers and their families at current wage levels). If the Subcommittee is serious about getting people to work their way out of poverty, it must give them the tools to do so, which means paid educational opportunity.

Providing minimum wage pay to attend school will assure that, when the wage is increased, those without skills will not be priced out of the economy - as some fear when opposing raising the wage. One reason to raise the minimum wage is precisely so no one lives only on their child tax credit proceeds. There are some in both parties who believe that the child tax credit should have a work requirement. I agree if that work includes being paid to go to school.

Paid training must be provided to those whom the education system and the former culture of dependency has failed. The caricature of the welfare cheat was never reality, however those who were and are trapped in poverty usually have educational deficits, as well as a history of family incarceration due to the war on drugs and its disproportionate penalties for Black and Hispanic men.

Paid training must not only make failed students whole, but advance all students to either vocational training or the completion of the first two years of college (both community and residential). Students with families would also receive the child tax credit. In either case, wages, the CTC payment, health insurance (rather than Medicaid) and any social services, should be delivered through the training provider.

English as a Second Language should not only be free, but workers should be paid to attend, irrespective of immigration status. Part-time workers should also be eligible for this benefit.

Technical training should be covered as well at both public and accredited private schools, including religious schools. In Espinoza v. Montana, prohibitions on funding private schools (Blaine Amendments) were found to be unconstitutional. New (and existing) funding should reflect that fact.

The homeless find it impossible to get jobs and hard to get benefits. This is why the “housing first” approach is essential to getting people back into the workforce or to channel them into the appropriate educational program - including those associated with drug court and disability insurance. Such individuals should be required to attend either long term recovery programs, occupational therapy or psychiatric rehabilitation programs - but be paid to do so.

With a higher minimum wage, payment for training and rehabilitation and a decent sized child tax credit, housing will be affordable without additional subsidies (save possibly for those with permanent disability - but even they should be paid to attend training and such training should not be time limited by payment through Medicaid).

What will society gain for all of this generosity, aside from higher economic growth? This should be obvious - indeed, it has even been proposed by the Senator from Utah - albeit clumsily. Food Stamps, TANF and even Medicaid for the non-elderly poor, as well as governmentally provided case management could be abolished in the vast majority of cases. Dependency would not only end - it would be both impossible and unnecessary.

To encourage work in good jobs, unemployment insurance must be less punitive, particularly where younger workers are concerned. In lower wage jobs, the preference is to find potential supervisors (whose compensation is usually subpar as well) and keep a file of infractions to justify firing workers who do not work out. A punitive work environment that does not exactly make any kind of work attractive.

In certain circumstances, unemployment compensation should be available on a no-fault basis. Better still, employees should be allowed to voluntarily leave firms with a history of quickly dismissing employees without penalty. There should be no expendable jobs or workers.

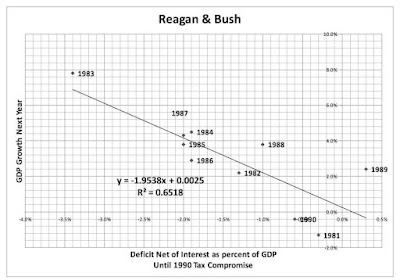

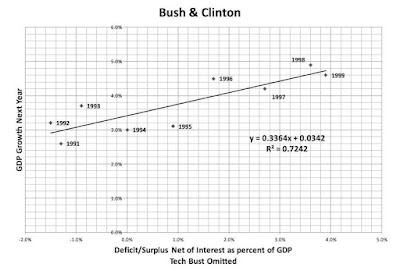

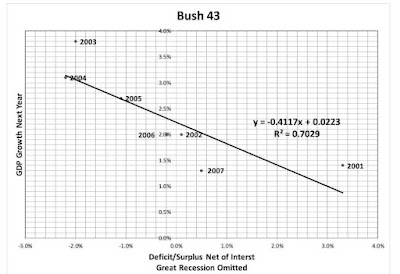

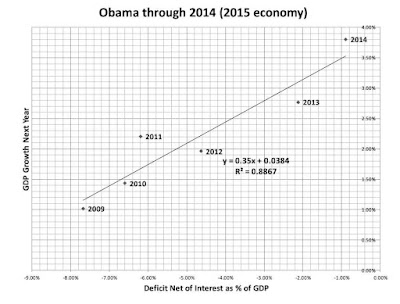

Lastly, to make work pay better for everyone, quit overpaying the few through inflation adjustments. Households making under the 90th percentile have been losing ground for almost half a century,while incomes above that amount have increased on a regular basis.

The source of inequality, aside from abandoning the 91% top marginal tax rate, is granting raises at an equal percentage rather than by an equal amount. When the 91% rate was repealed, incomes were fairly equal, so it was not an issue.

The federal government plays an outsized role in how salaries are determined through percentage based cost of living adjustments to government workers, beneficiaries, government contractors. The government can change this with the stroke of a pen. The private sector will follow suit with a higher minimum wage, adequate child tax credits (as described below) and paying individuals in training from ESL to community college the minimum wage to purse their studies.

From here on in, adjust for cost of living on a per dollar an hour rather than on a percentage basis (or dollars per month or week for federal beneficiaries). Calculate the dollar amount based on inflation at the median income level. No one gets more dollars an hour raise, no one gets less dollars per hour in increases. Increase the minimum wage as above and consider decreasing high end salaries paid to government employees and contractors. Even without decreases, simply equalizing raises will soon reduce inequality. Why is this necessary?

Prices chaise the median dollar. The median dollar of income is actually at the 90th percentile, rather than the 77th percentile (which is about where the median is). This strategy will reduce inflation in both the long and short terms as prices adjust to decreases in higher salaried income. Let me repeat this - prices chase income dollars, not income earners.

Attachment: Tax Reform Videos included